1 Introduction

There have been recent amendments to the Stamp Duty Law of Cyprus (Law 19/1963) (the “Law”) with the aim of modernising and simplifying the Law. The main amendments relate to the rates of stamp duty payable for different types of documents.

2 Scope of the Law

2.1 The Law provides that all documents which are specifically set out in Schedule 1 of the Law are subject to stamp duty if they relate to:

2.1.1 any property situated in Cyprus; OR

2.1.2 matters or things which are done or executed in Cyprus irrespective of the place where they have been prepared.

2.2 In case, with respect to a contract or arrangement, more than one document is entered into (either at the same time or at different times), only the main document is subject to the normal rate of stamp duty and the rest of the documents are subject to a duty of €2 each.

3 Timing for payment of stamp duty

3.1 The Law provides that a document which is subject to stamp duty can be stamped and the relevant duty paid, without any penalties, prior to or within 30 days from the date of its signing (or 30 days from the date the document (or any physical or electronic copies of the same) are brought to Cyprus, if executed abroad).

3.2 It is also possible to stamp a document within six months from the date of its signing, although penalties will be payable as follows:

3.2.1 in case the unpaid duty does not exceed €2, by paying the unpaid duty plus a penalty of €2;

3.2.2 in case the unpaid duty is between €2 and €35, by paying the unpaid duty plus a penalty equal to the amount of duty not paid;

3.2.3 in case the unpaid duty exceeds €35, by paying the unpaid duty plus a penalty of €35 plus 10% of the unpaid amount over €35.

3.3 It is even possible to stamp a document after the passing of six months from the date of its signing by paying the unpaid duty plus a penalty twice the amount of the penalties referred to in paragraph 3.2.

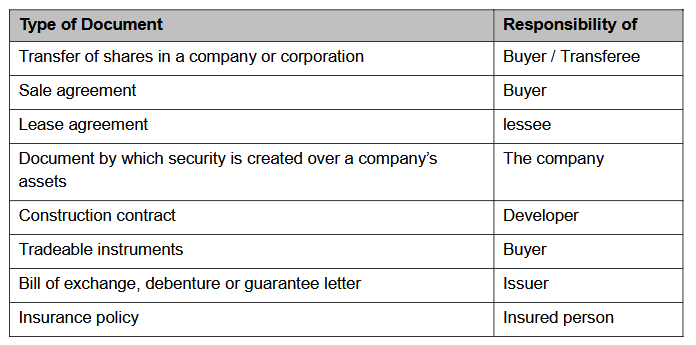

4 Responsibility for payment of stamp duty

In the absence of an agreement to the contrary, the responsibility for payment of stamp duty is as follows

5 Consequences of not paying stamp duty

The consequence of not paying the relevant stamp duty with respect to a document is that such document is not admissible as evidence in court unless payment of the duty (and appropriate penalties) is made.

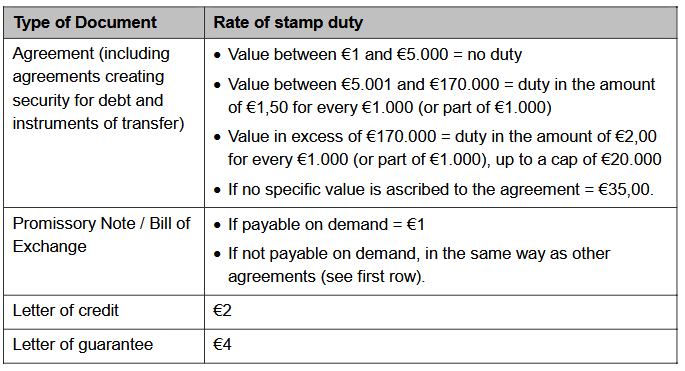

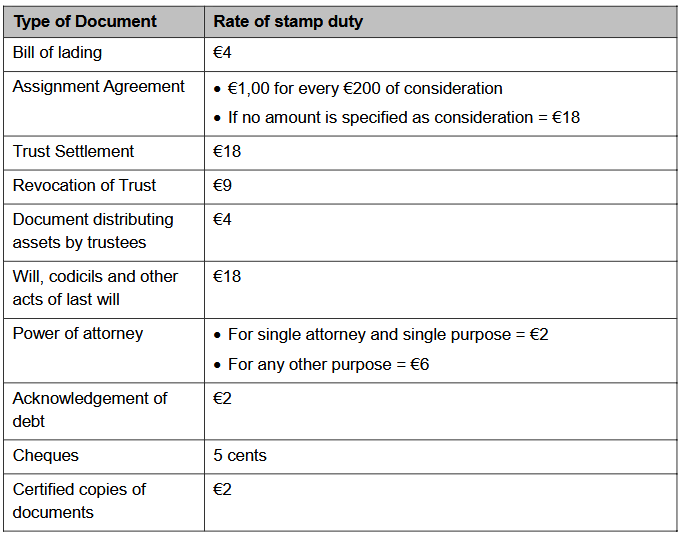

6 Stamp Duty Rates

The rates of stamp duty are set out in detail in Schedule 1 of the Law. The rates of key types of documents are set out below:

7 Notable exceptions

The following are the most material exceptions to the general rule on stamp duty, as provided in the Law itself:

(i) agreements, mortgages or other documents which are executed within the framework of debt restructuring;

(ii) agreements for the sale of goods;

(iii) ship sale agreement or any agreement for purchase of part of a ship or interest in a ship; and

(iv) transactions relating to transfer of shares traded in any recognised stock exchange.

Key Contacts

For further information, please contact:

Pavlos Kaimakliotis

Partner

Tel: +357 24 01 01 01

pavlos.kaimakliotis@kaimakliotis.com