Cyprus Taxation: Introduction of non-domicile rules for individuals

1 Introduction

Under the amendments to the Special Contribution for the Defence of the Republic Law (“SDC”) which have been introduced in July 2015, tax authorities in Cyprus impose tax on income deriving from rent, interest and dividends that is received by persons who are (subject to exemptions) both (i) Cyprus tax residents and (ii) domiciled in Cyprus. The introduction of the latter condition (the “non-dom rule”) has created significant tax incentives to individuals who consider taking up residency in Cyprus (while not domiciled there), especially corporate executives and high-net-worth individuals.

2 Who is considered a tax resident of Cyprus and/or domiciled in Cyprus

2.1 Generally a person is considered to be a resident of Cyprus for tax purposes if that person is physically present in Cyprus for an aggregate period of 183 days or more during a calendar year.

2.2 An individual is considered to be domiciled in Cyprus for the purposes of SDC if:

2.2.1 he/she has a domicile of origin in Cyprus (this is generally the domicile of the individual’s father at the time of birth (subject to certain exemptions) per the Wills and Succession Law of Cyprus); or

2.2.2 if he/she has been a tax resident in Cyprus for at least 17 out of the 20 tax years immediately prior to the tax year of assessment.

3 Effect of non-dom rule

3.1 The effect of the introduction of the non-dom rule is essentially that an individual Cyprus tax resident who is a non-dom person will not be subject to SDC in Cyprus and therefore will not be subject to SDC tax on:

3.1.1 rental income (otherwise subject to 2.25 of the rental income);

3.1.2 passive interest income (otherwise subject to 30% tax); and

3.1.3 dividends income (otherwise subject to 17% tax), irrespective of the fact that such income may be derived from sources in Cyprus and/or remitted to a Cypriot bank account or used or spent in Cyprus.

3.2 Given also that income from dividends (either from Cyprus or overseas), interest and rent is fully exempt from Income Tax in Cyprus, worldwide income from these sources is totally exempt from tax in Cyprus.

4 Other tax incentives for foreign individuals to relocate to Cyprus

Aside from the benefits of the non-dom rule, there are a number of other tax incentives which a foreign individual relocating to Cyprus may benefit from.

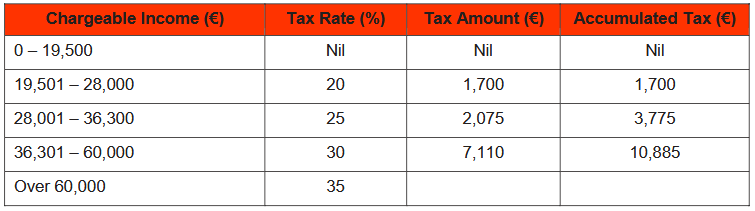

4.1 Relatively Low Personal Income Tax

Personal Income Tax rates are among the lowest in the EU. They range between 0% and 35% (with the first €19,500 being exempt). The rates are as follows:

4.2 Relief for high-earners taking up employment in Cyprus

4.2.1 A non-resident individual who relocates to Cyprus and takes up employment in Cyprus with an employment income in excess of €100,000 per annum benefits from a 50% exemption on Personal Income Tax relating to this employment income for a period of 10 years, starting from the year after the first year of relocation. In addition social insurance payments are also one of the lowest in Europe with social insurance deductions of 7.8% for the employee and 11.5% for the employer with a maximum insurable amount of €54,396.

4.2.2 If the individual’s income from employment is less than €100,000 and therefore the exemption in paragraph 4.2.1 does not apply, such person will nevertheless benefit from a 20% exemption on his employment income (up to a maximum amount of €8,550). This exemption applies for a period of five years but it can only be claimed until the year 2020.

4.3 Exemption for employment income from working abroad

A Cyprus tax resident benefits from a 100% exemption from income from employment with respect to services rendered outside of Cyprus for a period in excess of 90 days per tax year to (i) a non- Cyprus resident employer or (ii) to a foreign permanent establishment of a Cyprus resident employer.

4.4 Taxation of pension receipts attributable to past employment

A Cyprus tax resident receiving pension income attributable to past employment will be taxed in Cyprus at a rate of only 5% on amounts in excess of €3,420.

4.5 Other tax benefits

An individual relocating to Cyprus will also benefit from all other tax advantages available to Cyprus tax residents, which include the following:

• no estate duty, wealth tax, inheritance tax or gift taxes;

• 100% exemption on the entire amount gained from the disposal of titles such as shares, bonds, debentures, futures, options and others;

• no Capital Gains Tax on the sale of immovable property situated out of Cyprus; and

• no Capital Gains Tax from the sale of immovable property situated in Cyprus which was acquired between 16/07/2015 and 31/12/2016.

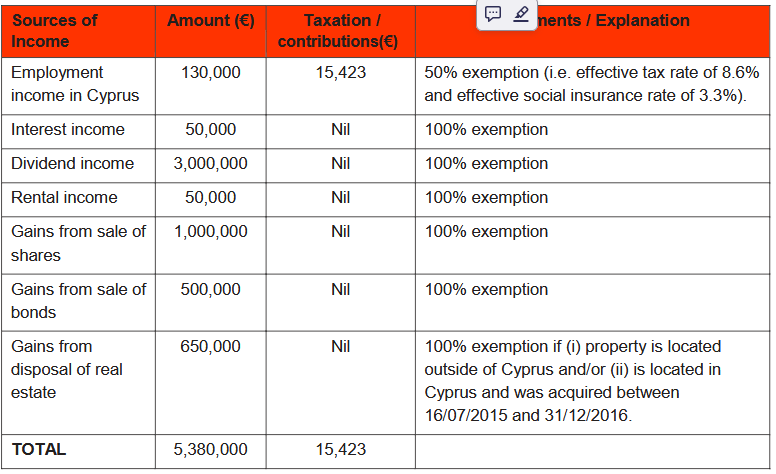

5 Worked Example of taxation of a non-dom Cyprus tax resident

6 Conclusion

6.1 It is therefore clear that an individual relocating to Cyprus can utilise the non-dom and other tax

advantageous rules and stands to obtain significant tax benefits.

6.2 But it’s not only tax and monetary benefits which are gained when relocating to Cyprus. Individuals

can enjoy:

• World-class education system

• Highly-skilled work force, including a competitive professional services and banking industry

• Most people speak English

• Over 325 days of sunshine per year

• Unique history and culture

• Easy connection and access to European destinations

• Among the lowest crime rates in the world

Key Contacts

For further information, please contact:

Pavlos Kaimakliotis

Partner

Tel: +357 24 01 01 01

pavlos.kaimakliotis@kaimakliotis.com

Koula Fili

Counsel

Tel: +357 24 01 01 03

koula.fili@kaimakliotis.com